Earned Wage Access: A Practical Tool for Supporting Members Between Paychecks

For many working Americans, income is not the biggest obstacle to financial stability; it’s timing.

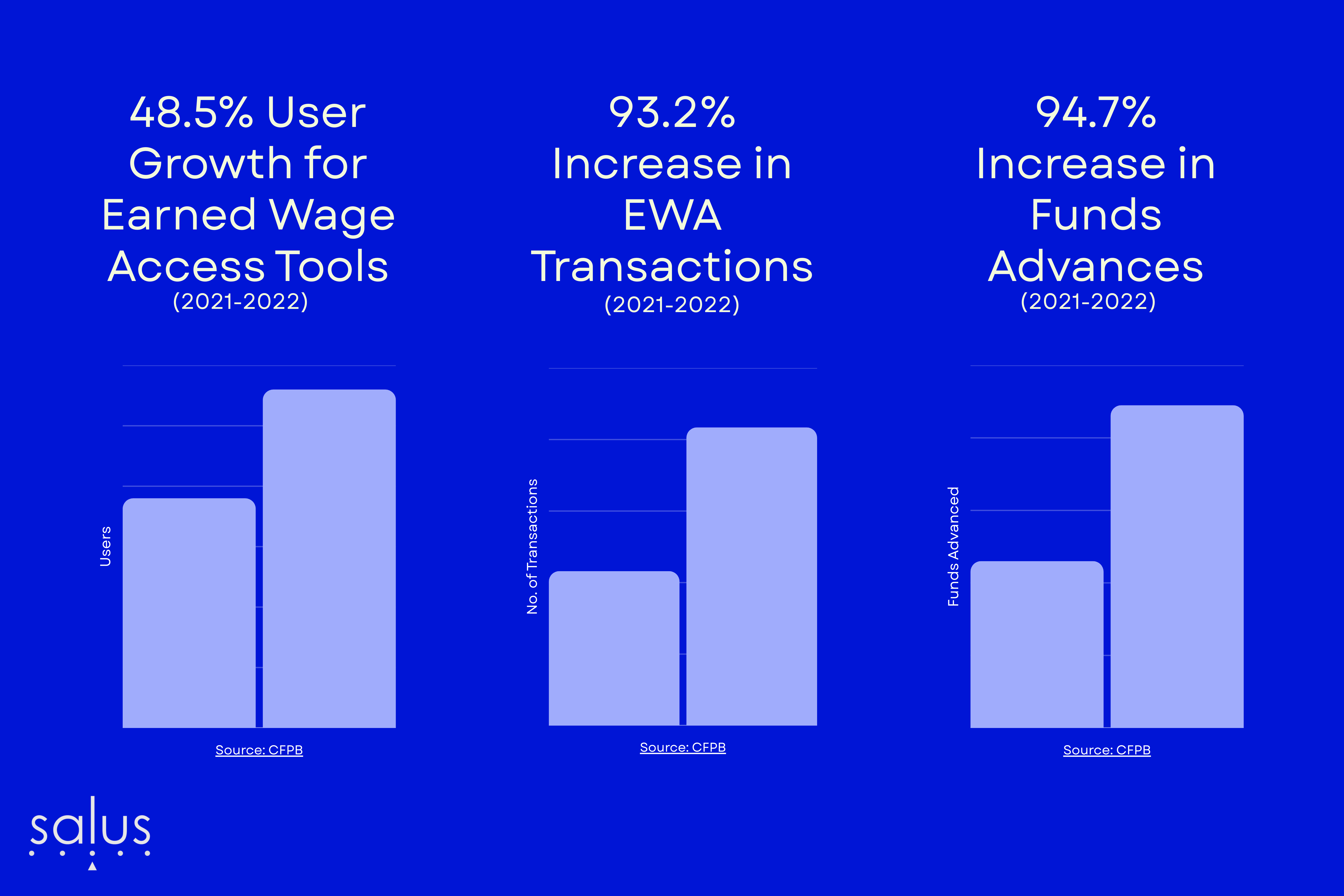

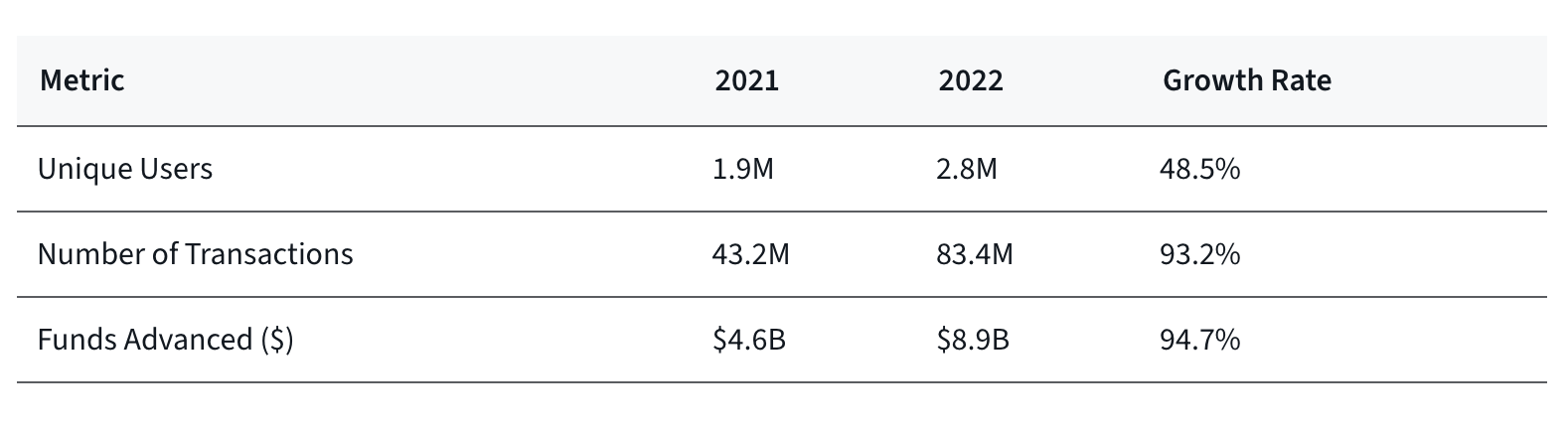

According to the Consumer Financial Protection Bureau, employer pay advance usage has skyrocketed. The number of transactions and the funds advanced nearly doubled, while unique users grew by nearly half. The average size is actually relatively small – less than $200.

CFPB’s research found that employees, on average, took 27 earned wage transactions per year. The share of workers who used the product at least once a month grew to 50% in 2022. The demand is there.

Otherwise, employees often resort to overdrafts, high-cost payday loans, title lenders, or credit cards, which might come with high fees and long-term financial consequences. As a credit union executive, you’ve likely seen the ripple effects of this on your members in the form of missed loan payments, overdrafts and NSFs that hurt both member well-being and your loan portfolio performance.

Earned wage access offers a smarter, more compassionate solution. And it aligns closely with credit unions’ mission.

What Is Earned Wage Access?

EWA allows members to access a portion of their already earned wages before their scheduled payday. It's not a loan; there’s no interest, no credit check and no repayment obligation. Instead, it gives members timely access to the money they've already earned, helping them avoid financial shortfalls between paychecks.

EWA funds can be deposited directly into a member’s credit union account, providing frictionless speed and convenience. Plus, Salus can do the heavy lifting for your credit union.

Why It Matters for Credit Unions

While EWA is gaining popularity among fintechs and neobanks, credit unions are uniquely positioned to offer it with member-first values and pair it with financial coaching. Here’s why EWA should be on your radar:

1. It supports member liquidity without increasing debt. EWA helps your members avoid harmful alternatives like payday loans or pawn shops. According to Payroll.Org, 78% of Americans are living paycheck-to-paycheck, and 34% would like earlier access to their wages.

2. It strengthens your credit union’s competitive position. With large banks and digital-first providers offering EWA options, members may look elsewhere if you can’t meet the same expectations. Offering EWA helps position your credit union as both modern and mission-driven.

3. It improves member retention and engagement. Almost all, 93%, of users feel in control of their finances, a 21-basis point jump from before they used earned wage access, according to FTI Consulting. Additionally, a significant number said it boosted their mental health. This product is aligned with holistic wellness and helps you make members for life.

What’s the Risk?

If your credit union requires direct deposit with the product, there is minimal risk. Income volatility (rather than earning a low income) is one of the top predictors of financial stress and default on other loans. By helping members smooth income timing, EWA can reduce financial stress and improve overall repayment behavior.

Plus, tools like real-time portfolio monitoring and predictive analytics, like Salus’ Predictive Analytics (Sentinel), help you track how EWA users perform across your portfolio and identify potential risks early. When you know the bigger picture, you can proactively reach out with assistance, before it’s too late.

How Salus Helps Credit Unions Offer EWA Responsibly

At Salus, we help credit unions offer Earned Wage Access as part of a broader strategy to attract and retain younger members, support financial wellness and reduce credit risk.

Our platform integrates seamlessly, so your credit union can be your members’ hero! It monitors usage, so you can see how EWA affects risk and provides predictive insights to flag early signs of financial stress. Plus, you can segment your members for a more personalized financial education experience.

At its core, EWA is about giving members control over their money. It respects their autonomy, reduces reliance on predatory lenders and offers timely support in a way that aligns with credit unions’ people-helping-people philosophy.

It’s not charity. It’s innovative financial design.

And when paired with responsible monitoring and proactive member support, it can help reduce delinquencies, boost member loyalty and position your credit union as a modern, tech-savvy financial partner in your members’ financial lives.

If you’re ready to explore how earned wage access fits into your credit union’s financial wellness strategy, Salus is ready to help.

Let's Start Making Members For Life