7 Banking & Financial Priorities for Gen Z Credit Unions Need to Know

As Gen Z (born between 1997 and 2012) steps into adulthood, their unique financial behaviors and preferences are reshaping the banking landscape. For credit union executives, this presents both challenges and opportunities. By aligning services with Gen Z's values and expectations, credit unions can position themselves as the preferred financial institutions for this emerging demographic.

1. Young adults are redefining success

According to Intuit’s 2025 Prosperity Index:

· 60% of young adults favor higher quality of life over greater wealth

· Gen Z leads with 64% prioritizing peace of mind over money

· 62% responded that they want more personal time and flexibility rather than a higher income

That suggests that talking about savings and budgeting for an experiential purpose might be in order. For example, credit unions might bring back a modern version of the old vacation accounts.

2. Diversifying income streams

Facing economic volatility, many Gen Z individuals are diversifying their income sources. More than 56% aim to establish two to three income streams within the next five years, with approximately 25% already claiming side hustles.

Credit unions can support this entrepreneurial spirit by offering flexible financial products and services tailored to gig workers and freelancers. Early access to their invoices (wages) based on certain criteria should also be a consideration. Additionally, tax help also could be an extra benefit for all those 1099s.

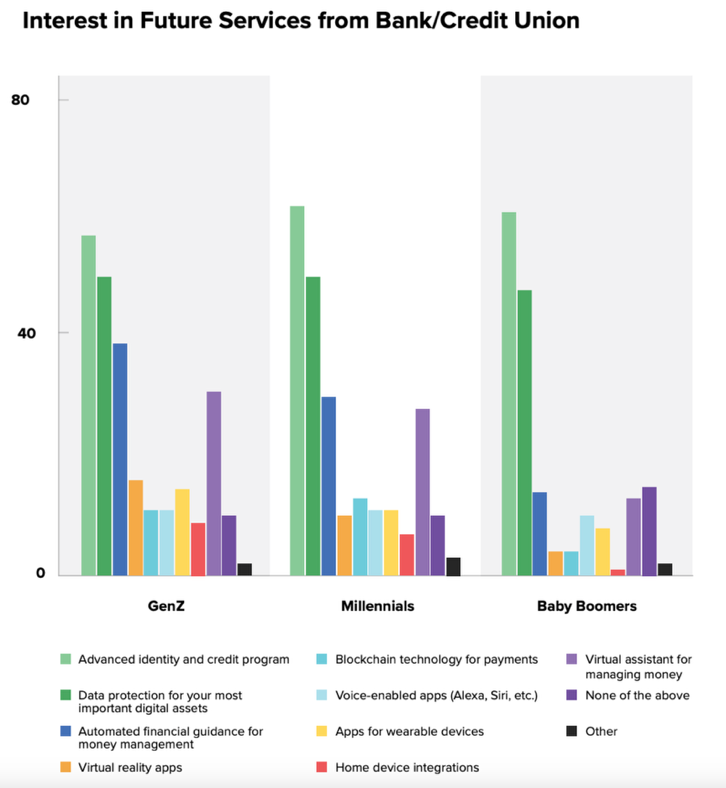

3. Digital-first banking preferences

Credit unions have relied on their in-person service for decades, but the COVID pandemic turned our world upside down. Now, just 4% of Gen Z (who were in high school during the pandemic) and millennials prefer in-person banking, according to Bankrate.com. Even older generations made the shift to digital and many stuck with it.

The big split comes with mobile banking. Nearly half (45%) of millennials and Gen Z bank exclusively digitally. However, only 8% of Gen Z and 12 % of millennials primarily use digital banking; most (64% and 60%, respectively) primarily use mobile banking.

This digital-first movement caught traditional financial institutions on their heels. Less than half (47%) of Gen Zs surveyed had accounts at a traditional bank or credit union, neobank or fintech. Compare that with 75% of baby boomers and even 70% of millennials. Branches are still critical for older generations and even younger ones in certain consultative situations, but member service investments should shift with the changing demographic tides.

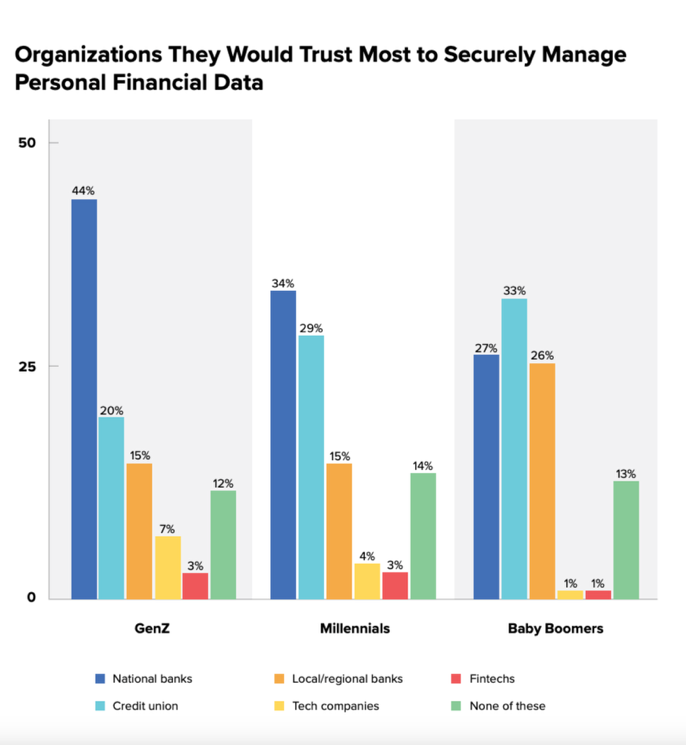

While there are services Gen Z wants from their bank or credit unions, the real kicker is that they don’t trust credit unions or community banks as much as big banks to keep their data safe.

4. Young people are highly fee-sensitive

Transparency and fairness in fees are crucial for retaining Gen Z members. A 2025 J.D. Power study found that 31% of credit union members under 40 would likely abandon their institution if they’re hit with unexpected fees. Ensuring clear and transparent communication about fees in a manner in which they’ll be more likely to see it is crucial to keep them coming back to your credit union. Think about offering low- or no-fee accounts to build trust with Gen Z and millennials.

5. Values alignment is essential

Gen Z tends to distrust traditional financial institutions, viewing them as profit-driven and misaligned with their values. However, credit unions’ not-for-profit, community-focused, member-first approach resonates with Gen Z’s desire for authenticity and social responsibility. Emphasizing common values in marketing, public relations and member engagement can strengthen your credit union’s bonds with Gen Z.

6. Enhancing Financial Literacy

Many Gen Z individuals face financial challenges, including student loan reporting to credit bureaus and credit card debt averaging $2,834—26% higher than millennials a decade ago. Credit unions can play a pivotal role by offering financial counseling programs, budgeting tools and personalized financial advice to help Gen Z manage debt and build financial stability.

Additionally, millennials are discovering exactly how difficult adulting is. Research from Alkami, Generational Trends in Digital Banking Study, found that 73% of millennials say higher interest rates have affected their standard of living significantly; 65% said they are living paycheck-to-paycheck. They need sound advice and counseling to make the life-changing financial decisions they’re facing, from when to buy a home to investing for the long term. Providing essential financial planning tools and educational opportunities will help build trust and lifetime member value.

7. Capitalizing on Top-of-Wallet Opportunities

Credit unions are making progress toward the coveted primary financial institution status for Gen Z, “signal(ing) a dramatic validation of credit unions’ evolving value proposition.” A recent study revealed a 60% top-of-wallet conversion rate among Gen Z consumers – a much-needed victory for credit unions over traditional banks and digital-only institutions. By continuing to innovate and align services with Gen Z's wants and needs, credit unions can move the needle toward becoming the go-to financial partner for this generation.

Conclusion

Gen Z’s financial behaviors reflect a generation seeking purpose, balance and digital convenience. Credit unions that adapt genuinely to these preferences, such as enhanced mobile services, financial counseling and fee transparency, will be well-positioned to capture the hearts, minds and wallets of Gen Z. Ensuring your credit union remains relevant for young adults will help ensure its long-term viability despite your digital-first competitors.

Let's Start Making Members For Life